You are currently browsing the category archive for the ‘Global Crisis Blog’ category.

Why Rwanda Is Far Smarter Than the US –

Dealing with COVID-19

By Shlomo Maital

Consider Rwanda. This small African country in south-central Africa, landlocked, has about 12 million people, with GDP per capita of about $2,600. This is only 4% of America’s per capita GDP. So Americans are 25 times wealthier than Rwandans…. But – is the US leader as smart as Rwanda’s, Paul Kagame? 4% as smart?

Rwanda has struggled to move beyond the terrible massacre/genocide that occurred between April and July 1994, which killed between half a million and a million Tutsi – 70% of the total Tutsi population in Rwanda.

Here is how Jason Beaubien, National Public Radio, described Rwanda’s success in controlling COVID-19. First the numbers:

| Cases

4,789 |

Recovered

3,080 |

Deaths

29 |

Now Beaubien:

“A robot introduces itself to patients in Kigali, Rwanda. The robots, used in Rwanda’s treatment centers, can screen people for COVID-19 and deliver food and medication, among other tasks. The robots were donated by the United Nations Development Program and the Rwanda Ministry of ICT and Innovation.

“In some places in the world right now, getting tested for COVID-19 remains difficult or nearly impossible. In Rwanda, you might just get tested randomly as you’re going down the street.

“So whenever someone is driving a vehicle, bicycle, motorcycle or even walking, everyone is asked if you wish to get tested,” says Sabin Nsanzimana, director general of the Rwanda Biomedical Center, which is the arm of the ministry of health that’s in charge of tackling COVID-19. Health officials in personal protective equipment administer the test. Nsanzimana says the testing is voluntary, although some others say refusal is frowned upon.

“The sample collection — from a swab up the nose — and filling out the contact information paperwork takes about five minutes.

“All these samples are sent that day to the lab,” Nsanzimana says. “We have a big lab here in Kigali. We have also six other labs in the other provinces.”

“Despite being classified by the World Bank as a low-income country, and despite its limited resources, Rwanda has vowed to identify every coronavirus case. Anyone who tests positive is immediately quarantined at a dedicated COVID-19 clinic. Any contacts of that case who are deemed at high risk are also quarantined, either at a clinic or at home, until they can be tested.

Kagame is controversial; he is accused of being dictatorial and anti-democratic. That may be. But he and his country have done much much better than the wealthy United States, in protecting its citizens.

Remember what President Trump called some African countries? In 2018? S???hole countries? Hmmm.

SARS-COV-2 Has One Big Trick – Have We Just Discovered It?

By Shlomo Maital

According to the India Times’ Economic Times: SARS-COV-2 virus has one big trick – and it may be that scientists have just figured out what it is.

“It looks like this virus has one big trick,” said Shane Crotty, a professor in the Center for Infectious Disease and Vaccine Research at the La Jolla Institute for Immunology in California. “That big trick is to avoid the initial innate immune response for a significant period of time and, in particular, avoid an early type-1 interferon response.”

According to the India Times: The work highlights the potential for interferon-based therapies to enlarge a slowly accumulating range of Covid-19 treatments. These include Gilead Sciences’ remdesivir and convalescent plasma, a component of the blood of recovered patients that may contain beneficial immune factors. These treatments provide limited benefit and are typically used in very sick, hospitalized patients. The possibility that interferon may help some people is enticing because it appears most efficacious in the early stages of infection when life-threatening respiratory failure could still be averted. Dozens of studies of interferon treatment are now recruiting Covid-19 patients.

How did the scientists figure this out? Here is the story:

When two brothers fell critically ill with Covid-19 around the same time in March, their doctors were baffled. Both were young — 29 and 31 years old — and healthy. Yet within days they couldn’t breathe on their own and, tragically, one of them died. Two weeks later, when a second pair of Covid-stricken brothers, both in their 20s, also appeared in the Netherlands, geneticists were called in to investigate. What they uncovered was a path leading from severe cases, genetic variations and gender differences to a loss of immune function that may ultimately yield a new approach to treating thousands of coronavirus patients. The common thread in the research is the lack of a substance called interferon that helps orchestrate the body’s defence against viral pathogens and can be infused to treat conditions such as infectious hepatitis. Now, increasing evidence suggests that some Covid-19 patients get very ill because of an impaired interferon response. Landmark studies published on Thursday in the journal Science showed that insufficient interferon may lurk at a dangerous turning point in SARS-CoV-2 infections.

See also:

“Impaired type I interferon activity and inflammatory responses in severe COVID-19 patients” Science 07 Aug 2020: Vol. 369, Issue 6504, pp. 718-724

COVID-19 Vaccines: What We Know

By Shlomo Maital

In my country Israel, there are more new daily cases per million population than anywhere in the world. Europe too is undergoing a second wave; and many states in the United States are also seeing increasing morbidity. So – everywhere, we await a vaccine.

Over a hundred different efforts are underway to create, produce and administer COVID-19 vaccines. Here is what we know so far, based on a very clear, lucid website sponsored by the Children’s Hospital of Philadelphia. This vaccine effort is an amazing global effort, led by the top scientific minds, trying a wide variety of creative approaches, some tried and true, some radical and innovative. One or more of them will save humanity!

What types of vaccine are being tested?

Several.

* Inactivated vaccine — The whole virus is killed with a chemical and used to make the vaccine. This is the same approach that is used to make the inactivated polio (shot), hepatitis A and rabies vaccines;

*Subunit vaccine — A piece of the virus that is important for immunity, like the spike protein of COVID-19, is used to make the vaccine. This is the same approach that is used to make the hepatitis and human papillomavirus vaccines.

* Weakened, live viral vaccine — The virus is grown in the lab in cells different from those it infects in people. As the virus gets better at growing in the lab, it becomes less capable of reproducing in people. The weakened virus is then used to make the vaccine. When the weakened virus is given to people, it can reproduce enough to generate an immune response, but not enough to make the person sick. This is the same approach that is used to make the measles, mumps, rubella, chickenpox and one of the rotavirus vaccines.

* Replicating viral vector vaccine — In this case, scientists take a virus that doesn’t cause disease in people (called a vector virus) and add a gene that codes for, in this case, the coronavirus spike protein. Genes are blueprints that tell cells how to make proteins. The spike protein of COVID-19 is important because it attaches the virus to cells. When the vaccine is given, the vector virus reproduces in cells and the immune system makes antibodies against its proteins, which now includes the COVID-19 spike protein. As a result, the antibodies directed against the spike protein will prevent COVID-19 from binding to cells, and, therefore, prevent infection. This is the same approach that was used to make the Ebola virus vaccine.

* Non-replicating viral vector vaccine — Similar to replicating viral vector vaccines, a gene is inserted into a vector virus, but the vector virus does not reproduce in the vaccine recipient. Although the virus can’t make all of the proteins it needs to reproduce itself, it can make some proteins, including the COVID-19 spike protein. No currently licensed vaccines use this approach.

* DNA vaccine — The gene that codes for the COVID-19 spike protein is inserted into a small, circular piece of DNA, called a plasmid. The plasmids are then injected as the vaccine. No currently licensed vaccines use this approach.

* mRNA vaccine — In this approach, the vaccine contains messenger RNA, called mRNA. mRNA is processed in cells to make proteins. Once the proteins are produced, the immune system will make a response against them to create immunity. In this case, the protein produced is the COVID-19 spike protein. No currently licensed vaccines use this approach.

Which type of COVID-19 vaccine is most likely to work?

It is likely that more than one of these approaches will work, but until large clinical trials are completed, we won’t know for sure. Likewise, the different approaches may have different strengths and weaknesses. For example, mRNA or DNA vaccines are much faster to produce, but neither has been used to successfully make a vaccine that has been used in people. On the other hand, killed viral vaccines and live, weakened viral vaccines have been used in people safely and effectively for many years, but they take longer to produce.

In addition to differences in how long it takes to make different types of vaccines, each type may also cause the immune system to respond differently. Understanding the immune responses that are generated will be important for determining whether additional (booster) doses will be needed, how long vaccine recipients will be protected, and if one type offers benefits over another.

Is one of the COVID-19 vaccines expected be more effective for the elderly population?

It is likely that COVID-19 vaccines could have different levels of effectiveness in various subgroups of people. Because the elderly generally do not respond as well to vaccines, one or more COVID-19 vaccines may not work well for them, which is concerning given their higher risk of severe disease. The large phase III studies may not include people over a certain age. But, the manufacturers have been encouraged to include older people, so that we have this type of information earlier in the process than may usually occur. We will have to wait and see what the data show to know which vaccine(s) work best in the older population.

How many doses of a COVID-19 vaccine will be needed? Will a booster dose be needed?

The number of doses of a COVID-19 vaccine that will be needed has not yet been determined. The coronavirus vaccines being studied are evaluating one or two doses. When giving two doses, they are usually given one or two months apart. We will need to wait for the results of the clinical trials to have more information about how many doses will be needed.

How long will vaccine immunity last?

Since we do not yet know how long immunity after infection lasts, immunity following vaccination will also have to be determined. Likewise, immunity following vaccination will depend in part on which types of vaccines are licensed, what part of the immune system responds to the vaccine, and the level of immunity that is generated by the vaccine.

If more than one vaccine becomes available, could taking two different vaccines boost the effectiveness?

While it is likely that more than one COVID-19 vaccine will become available, we probably won’t have a good answer to this question until vaccines are actually licensed and we know more about them. Three scenarios can occur if a person is vaccinated with two versions of vaccines against the same disease, particularly close in time:

— They get a stronger immune response. An example of this was when children got inactivated polio vaccine and later got oral polio vaccine.

—- The second vaccine causes immunity that would be similar to receiving a second dose of the original vaccine. Using a different brand of hepatitis B vaccine for one or more doses would be an example of this.

— The immune response generated by the first vaccine interferes with components of the response to the second vaccine, in some cases causing lower immunity. For example, when people got a pneumococcal polysaccharide vaccine (PPSV) followed by a pneumococcal polysaccharide vaccine with a harmless helper protein attached to it, called pneumococcal conjugate vaccine (PCV), they had lower antibody responses to one part of the PCV vaccine than people who got the two vaccines in the opposite order (PCV followed by PPSV).

For these reasons, studies will need to be done to determine the effects of getting a second type of COVID-19 vaccine shortly after receiving a different one. If, however, we find that COVID-19 vaccines are like influenza vaccines and we need to get vaccinated annually, concerns about switching types from one year to the next are less likely to be an issue.

Will a coronavirus vaccine need to be given annually?

When a vaccine is licensed, we will only have information about length of immunity for as long as we are from the trials. For example, if the first people in the study were vaccinated in July 2020 and the vaccine is licensed in December 2020, we will only have information about the immune response up to 5 months after vaccination. The vaccine manufacturer will likely continue to monitor vaccine recipients for several months or more, so that over time, we will continue to get a better picture of the durability of immunity. With this information, we will be better able to understand whether vaccines against COVID-19 will require annual dosing like influenza.

Is a coronavirus vaccine necessary?

SARS-CoV-2 infections can be a minor hindrance or lead to severe disease or even death. While hygiene measures such as social distancing, handwashing, and wearing masks offer some help, the best way to stop this virus is to generate SARS-CoV-2-specific immunity. This specific immunity can be achieved in one of two ways — through illness or vaccination. Since illness could lead to severe disease or death, vaccination is a better alternative as long as safe and effective vaccines can be developed.

How long before a coronavirus vaccine takes effect?

Generally speaking, it takes a week or two for immunity to develop following vaccination, but the specific timeline for any coronavirus vaccine will depend to some extent on which type of vaccine is licensed. For example, a live, weakened vaccine requires time to reproduce in the body, whereas an inactivated vaccine is given at a dose that will generate immunity. On the other hand, because the live, weakened vaccine reproduces to generate immunity, it might provide a more robust immune response than an inactivated vaccine

Bad Weather Brings Flu – Makes Sense

By Shlomo Maital

The conflation of COVID-19 and the fall/winter influenza season worries public health officials. In Israel, hospitals are already over-stretched – and doctors and nurses dread the onslaught of flu patients, on top of several thousand new COVID-19 cases daily. This is why Israel is now in partial lockdown, during the High Holydays.

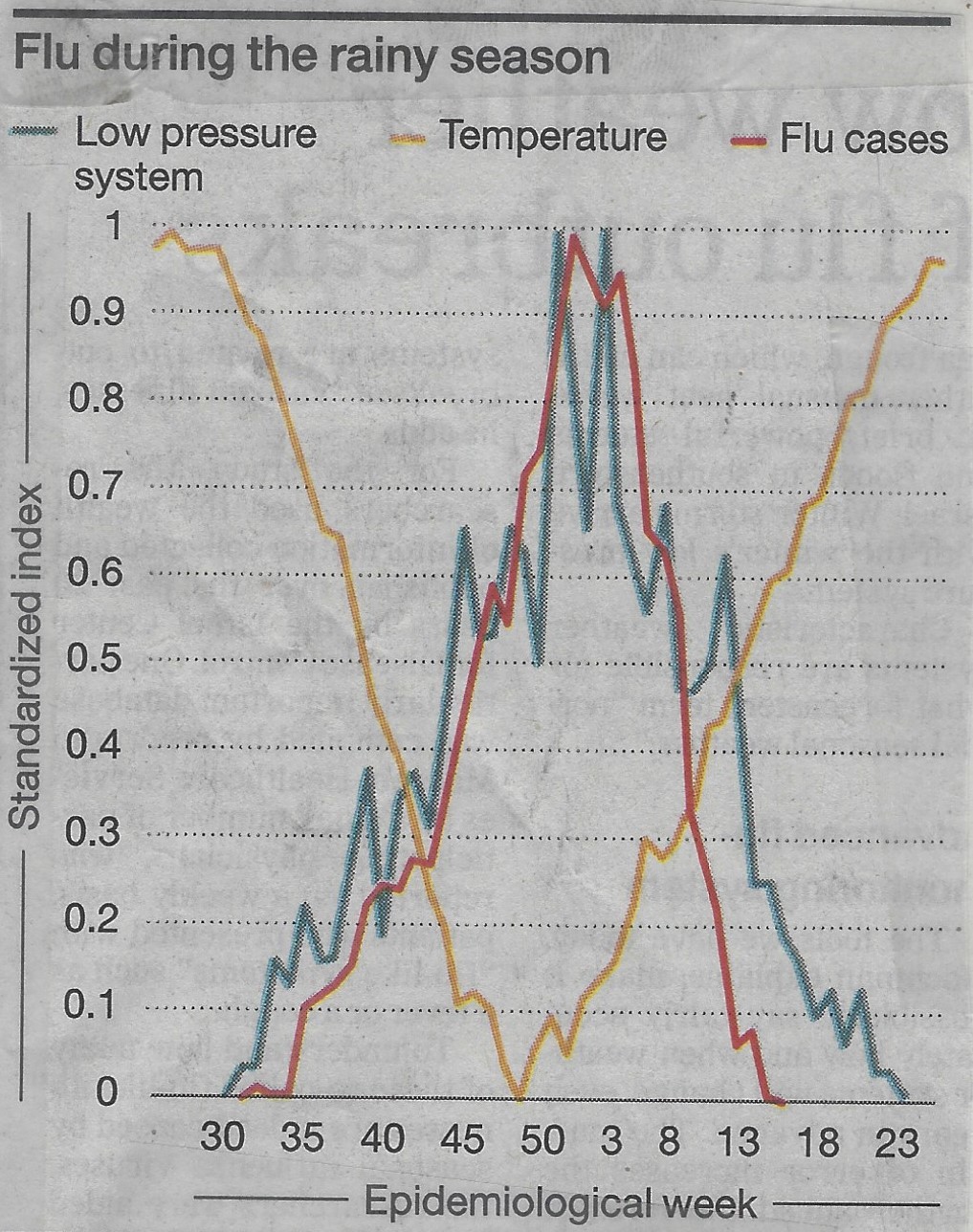

A new study by a group of Israeli and Mideast scholars shows, for the Eastern Mediterranean, a close correlation between climate and flu. *

The orange line above shows temperature. The red line: % of the population with flu. And the blue line: barometric pressure (inverted – high scale means low pressure). All three variables have been converted to a standardized zero to one normalized scale.

So – what is the connection between weather and flu?

It is pretty simple. Flu spreads through contact from one person to another. Outdoors, winds, even light breezes, disperse flu particles from sneezes and coughs and breathing. Indoors, this is far less true. In bad weather, people spend more time indoors. Hence, more flu.

This finding seems relevant for COVID-19 too. A friend of mine, a veteran pulmonary medical specialist, observes:

“With each cough and sneeze, there are very small particles under 10 microns in diameter, especially those under 2.5 microns, that tend to remain suspended in the air for a long time. This aerosol is scattered all over. While the volume of these particles is low, their surface area is large and lots of virus particles can stick to the surface of these small particles. It is now fully accepted that the virus’ transmission by aerosols is an important vector. The relatively large area of the eyes’ surface makes them vulnerable to the landing and culture of viruses. Protection against sprays and eye protection are crucial to creating barriers against contracting COVID-19.”

“Cough is the dominant mode of spread and as such should be monitored in areas where people congregate to assess risk in an objective mode and to identify possible spreaders. Cough monitoring is feasible with devices being available and used in pulmonary and occupational contexts.”

“The dilution in open air is immense. Consider the following example: A soft wind is blowing at 3.6 km/hour (2.2 miles per hour). If we consider a 4-meter- long test volume of air, the flow of air in the wind will sweep the test volume in four seconds, or nearly a thousand times per hour. This is significant and should be sufficient to prevent infection if very sporadic individuals are present. But if a distance of two meters cannot be observed at all times, the risk level is such that the use of a mask, at least surgical or cloth, is still required in the open.”

So, the message here is clear. We MUST get this second wave of COVID-19 under control before the flu season. If we don’t we will have two problems:

- Bad weather will bring influenza, and some flu sufferers will need hospitalization

- Bad weather will send people indoors, and COVID-19 spreads more easily there.

Hochman, A., Alpert, P., Negev, M., Abdeen, Z., Abdeen, A. M., Pinto, J. G., & Levine, H. (2020). The relationship between cyclonic weather regimes and seasonal influenza over the Eastern Mediterranean. Science of The Total Environment, 141686.

Ruth Bader Ginsburg – Words Matter

By Shlomo Maital

Ruth Bader Ginsburg in Israel

Do words really matter?

They do indeed. Especially when written by a diminutive Jewish woman, a Justice of the US Supreme Court for an entire generation.

Ruth Bader Ginsburg said this, about her class with famous Russian novelist Vladimir Nabokov, at Cornell University: (from a blog by Frances Katz):

“[Vladimir] Nabokov, changed the way I read and the way I write,” Ginsburg said. “Words could paint pictures, I learned from him. Choosing the right word, and the right word order, he illustrated, could make an enormous difference in conveying an image or an idea.”

She also says she always employs several of the lessons she learned in his class: “I seek the right word and word order,” she explained. “ And I use the ‘read aloud’ test to check whether I have succeeded.”

Rulings and dissenting opinions are first read aloud in court before being distributed to the public, so the ‘read aloud test’ helps her be certain the language be clear enough to articulate legal arguments but still be understood by ordinary citizens.

Her use of language is clear and direct. She redefines the issue and makes her argument. She calls on those who agree with her to push for change. She did not call on Congress directly, use inflammatory language or rhetorical flourishes. She chose her words carefully to make sure there was no misunderstanding her call for action.

One of her law clerks said yesterday on National Public Radio, that he worked hard on a legal opinion, and wrote 10 pithy pages. RBG complimented him, then took his draft and boiled it down to 3 and one half even more pithy pages, focused clear and powerful.

Words to matter. RBG’s words changed America and the world. She used the phrase “gender discrimination”, not “sex discrimination”, because the latter phrase, she knew, would not speak to the male Justices.

You CAN change the world, with the right words. And with stubborn persistence, and with, as she put it, the ability to “disagree without being disagreeable”.

Is COVID-19 Mutating? Yes – But Not Harmfully!

By Shlomo Maital

I’ve been worrying about whether the SARS-CoV-2 virus (the piece of RNA that gives people COVID-19) is mutating. Evolution is everywhere and inexorable, and it creates animals, insects and even viruses that are well adapted to survive and meet threats. So, I wondered, is the novel coronavirus mutating, to defeat our best efforts?

The answer is no. Here are answers from Dr. Edward Holmes, an evolutionary virologist at University of Sydney, in today’s New York Times.* I present his findings as Q&A:

- “The coronavirus is mutating, and that’s fine (so far).” NYT Sept. 14, p. 11.

Do viruses really mutate?

“Viruses routinely mutate — and most of these changes are bad for the virus or even fatal, according to some studies. (A minority of mutations are neutral, and only a tiny minority beneficial.) The word “mutation” may sound ominous, but it is a humdrum fact of viral life and its implications most often aren’t nefarious for humans.”

Has COVID-19 become more virulent, more dangerous?

“ The real question is this: Has it become more virulent or more infectious than it was when it was first detected in Wuhan, central China, in December? The evidence suggests that it has not. Like the viruses that give us influenza or measles, SARS-CoV-2 has a genetic code made up of RNA, or ribonucleic acid. But RNA is highly mutable, and since SARS-CoV-2 infects us by using our body’s cells to replicate itself again and again, every time its genome is copied, an error might creep in. Most mutations are quickly lost, either by chance or because they damage some part of the virus’s main functions. Only a small proportion end up spreading widely or lasting. Mutation may be the fuel of evolution but, especially for an RNA virus, it also is just business as usual.”

How fast is COVID-19 mutating?

“RNA viruses tend to evolve rapidly — about a million times faster than human genes. Yet if SARS-CoV-2 stands out among them, it is for evolving more slowly than many: about five times less rapidly than the influenza viruses, for example. According to Nextstrain, an open-source project that tracks the evolution of pathogens in real time, and other sources, SARS-CoV-2 is accumulating an average of about two mutations per month — which means that the forms of the virus circulating today are only about 15 mutations or so different from the first version traced to the outbreak in Wuhan. To my knowledge, there is to date no evidence that SARS-CoV-2 has become more virulent or more lethal — nor, for that matter, that it has become less so.”

Even if COVID-19 has not mutated to a more dangerous form, that kills more people – has it perhaps mutated to become more infectious – in a way Nature often does, to reproduce better? Is THIS perhaps why the coronavirus has created strong second waves in many countries?

“I do not believe that the evolution of SARS-CoV-2 is what’s driving the virus’s continued spread. The coronavirus remains good at propagating itself because most of us still are susceptible to it; we are not immune, and it can still find new hosts to infect relatively easily.”

Are you sure?

“There has been much discussion over whether the D614G mutation — which affects the so-called spike protein of the virus — has made SARS-CoV-2 more infectious. The spike protein sits on the surface of the coronavirus, and it matters because it’s the part of the virus that attaches to the host’s cells. “D614G” is shorthand for a change at position 614 of the spike protein, from an aspartic acid (D) to a glycine amino acid (G). (The technical literature refers to “D614” as the earlier configuration and “G614” as the later one.) The D614G mutation, which probably initially arose in China, first appeared to become more and more frequent in the outbreak in northern Italy in February. The G614 form of the virus has since spread all over the world and has become the dominant variant. The D614G mutation does seem to have increased the infectivity of the coronavirus — at least in cells grown in laboratories, according to a recent paper by the computational biologist Bette Korber and others published in the journal Cell.”

“Apparently based partly on this and other studies, health authorities in various countries have claimed that the G614 form of the coronavirus may be 10 times more infectious than the version first detected in Wuhan. But as some epidemiologists have warned, it is difficult, not to mention unwise, to extrapolate from lab results to explain how the virus actually spreads in a real population. In the issue of Cell …. the viral epidemiologist Nathan Grubaugh and colleagues argued that the “increase in the frequency of G614 could be explained by chance and the epidemiology of the pandemic.”

Bottom line?

“For now, though, SARS-CoV-2 essentially is the same virus that emerged in December. Sure, it has mutated, but not, so far, in ways that should change how scientists think about how to tackle it — and not in ways that should worry you.”

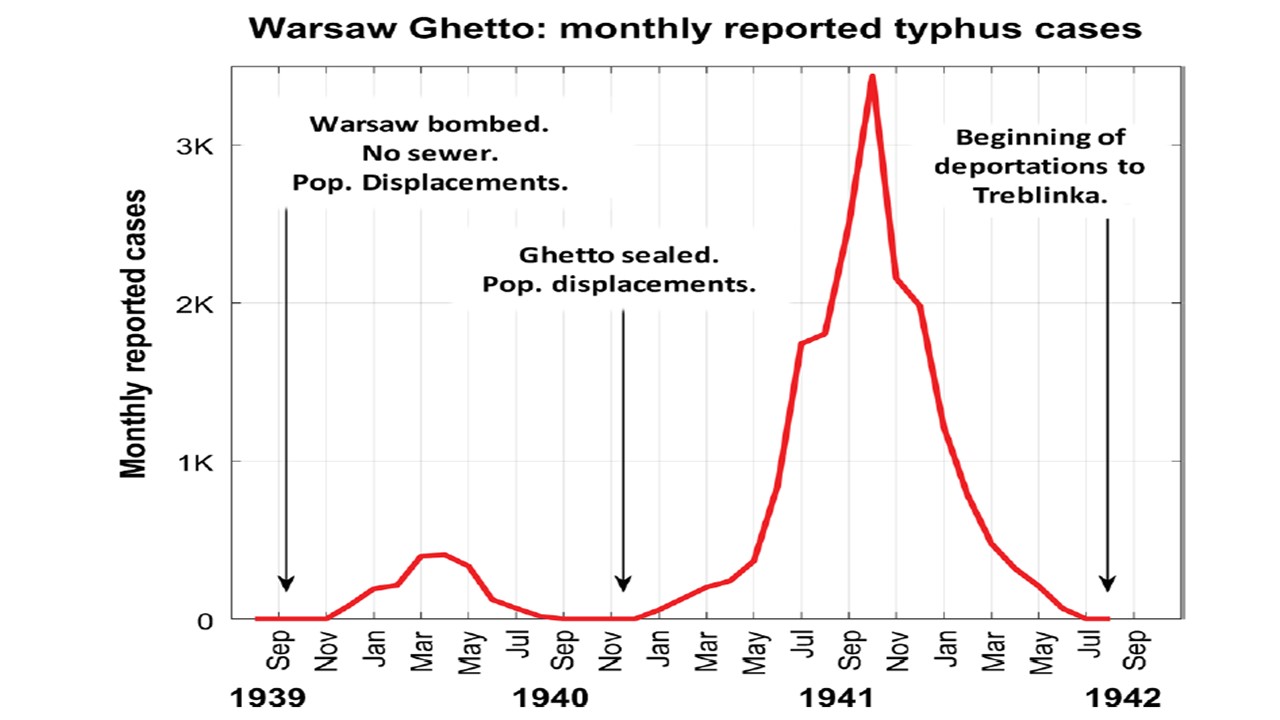

How Warsaw Ghetto Jews Controlled a Typhus Epidemic:

Lessons for Today

By Shlomo Maital

Typhus bacteria

This is the story of how 450,000 Warsaw Jews, crammed by the Nazis into a tiny ghetto 3.2 km. sq. (about 2 miles square, roughly Central Park) – starting in Nov. 1940 — and saw a typhus epidemic spread, with several thousand cases.. and then, by July 1942, totally flattened the curve and eradicated the epidemic. Right at that time, late 1942, the Nazis assaulted the ghetto, and despite valiant but futile resistance, destroyed the ghetto and transported its residents to Treblinka extermination camp, where more than 280,000 were killed.

So – what exactly is typhus, and how did the Warsaw Ghetto Jews flatten the curve?

Typhus is a group of infectious diseases — Common symptoms include fever, headache, and a rash. Typically these begin one to two weeks after exposure. The diseases are caused by specific types of bacterial infection. Epidemic typhus is due to Rickettsia prowazekii spread by body lice.

In a just-published article in Science Advances, theoretical biologist Lewi Stone and colleagues describe the Warsaw ghetto typhus epidemic, and how it was flattened (see graph above).

In brief: Among the Jewish doctors imprisoned by the Nazis in the ghetto were several distinguished epidemiologists, including one nominated for a Nobel Prize. The doctors told inhabitants to keep apart, and as far as possible practice body hygiene (the human body louse spreads the disease).

The ghetto inhabitants respected and trusted the doctors and did what they said. Authors of the study conclude: “Strangely, the epidemic was curtailed and was brought to a sudden halt before winter, when typhus normally accelerates. A far more massive epidemic outbreak was prevented through the antiepidemic efforts by the often considered incompetent and corrupt ghetto leadership and the Herculean efforts of ghetto doctors.

So – the starving inhabitants, weakened by hunger, lacking water, packed into housing like sardines — did manage to ‘flatten the curve’, almost to zero, at a time when typhus epidemics had ravaged and killed many, in other locations.

The question arises: If they could, if they did – why in the world can’t we? Why aren’t we?

- Extraordinary curtailment of massive typhus epidemic in the Warsaw Ghetto Lewi Stone, Daihai He, Stephan Lehnstaedt and Yael Artzy-Randrup. Science Advances, ci Adv 6 (30), eabc0927. DOI: 10.1126/sciadv.abc0927 Feb 2020

2,000-year-old dates: Delicious! Yum!

By Shlomo Maital

Credit: Dan Ballity, The New York Times

My story today begins nearly 2,000 years ago – around 73 CE — as Roman legions put a small group of die-hard 960 Jewish rebels under siege, in Masada, a mountaintop near the Dead Sea. The rebels commit suicide, every single one, rather than be taken prisoner by the Romans.

Archaeologist Prof. Ehud Netzer, excavating at Masada, is reported (according to the San Francisco Chronicle, in 2005) to discover data palm seeds, genus Phoenix dactylifera, discarded in a corner.

The ancient 2,000-year-old seeds are given to a botanist, Dr. Elaine Solowey, at the Arava Institute, located at Kibbutz Ketura, founded in 1973, in the Arava Valley north of Eilat. Solowey is the author of Supping at God’s Table: A Handbook for the Domestication of Wild Trees for Food and Fodder. Solowey and her colleagues embark on a Don Quixote mission: To germinate the seeds, grow them into a date palm tree – and harvest the fruit.

Really??? After two millenia?

Solowey treats the seeds with a growth hormone, gibberellic acid, researched at Yale in the 1960’s. The seeds are planted on Jan. 26, 2005. Amazingly, within five weeks, a seed sprouts to form a small tree! It is given a name: Methuselah Palm, after Methuselah, the son of Enoch, the father of Lamech, and the grandfather of Noah, in the Bible. Methuselah lived 969 years, the longest-lived person in the Bible. A good name!

Fast forward: New York Times correspondent Isabel Kershner reports in the Times, Sept. 8, p. 3, this:

“The plump golden-brown dates hanging in a bunch just above the sandy soil were ready to pick…..’They are beautiful!’ exclaimed Dr. Sarah Sallon [a medical doctor, from Hadassah Hospital, genetics expert, natural medicine researcher and part of the team], with the elation of a new mother, as each date, its skin slightly wrinkled, was plucked gently off its stem at a sunbaked kibbutz in southern Israel. ..They were tasty, too, with a fresh flavor that gave no hint of their two-millenium incubation period. The honey-blond, semi-dry flesh had a fibrous, chewy texture and a subtle sweetness. …These were the much-extolled, but long-lost Judean dates, and the harvest this month was hailed as a modern miracle of science.”

For Jews, it is possible one day to eat the same dates that the Masada rebels ate. For Christians, perhaps one day they will eat the same dates, the same flavor, texture, color, appearance, Judean dates, that Jesus ate.

And for the world — when the pandemic has made human civilization seem fragile, bumbling, and in great danger, we learn from the 2,000 year old dates how durable, adaptable and resilient Nature is, in its quest to endure and to prevail. And, as a footnote, how scientists can also prevail in quixotic quests that literally bear fruit.

For those who want to learn about the science see this article:

Sallon, S., Cherif, E., Chabrillange, N., Solowey, E., Gros-Balthazard, M., Ivorra, S., … & Aberlenc, F. (2020). Origins and insights into the historic Judean date palm based on genetic analysis of germinated ancient seeds and morphometric studies. Science advances, 6(6), eaax0384.

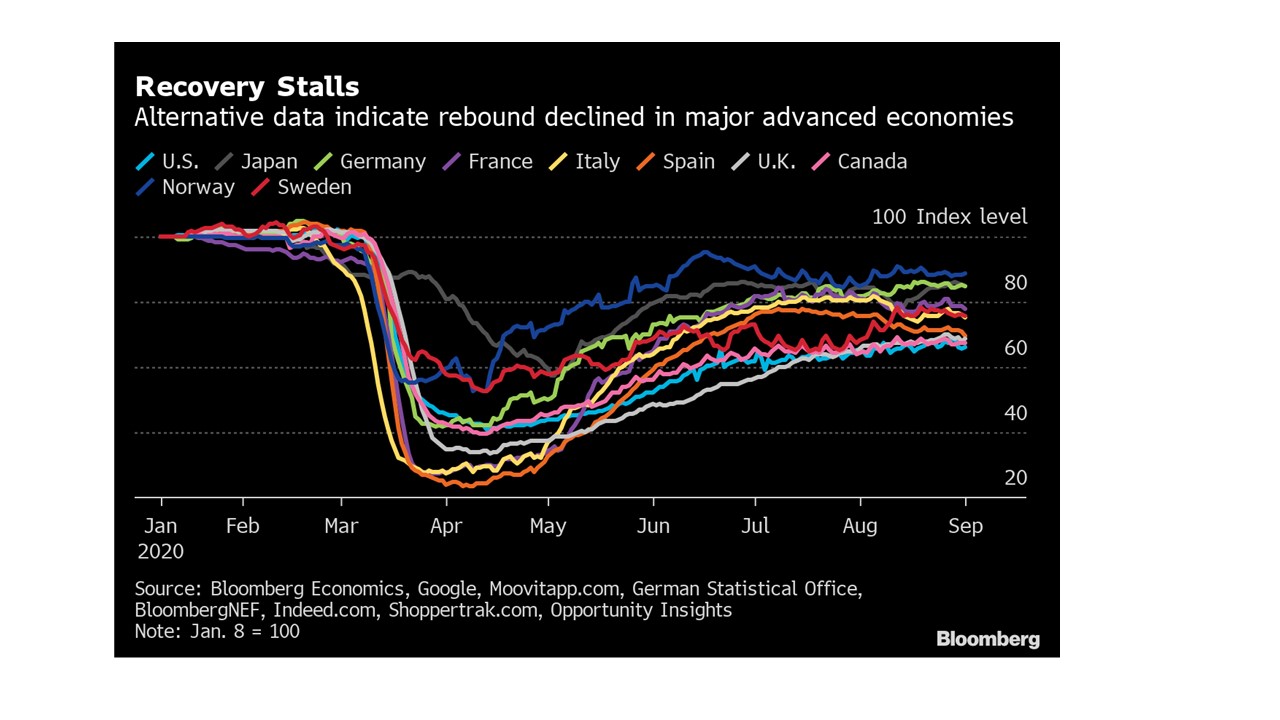

Economic Recovery: We All Should Prepare for a Long Convalescence

By Shlomo Maital

How quickly will economies in the US, Canada, Japan and Europe bounce back? Will it be fast, like China, or very slow, like the US?

Bloomberg has been tracking this key issue, using a wide variety of indicators; the visual track for 10 countries is shown in the diagram.

It has been 5 months since these economies bottomed out, with 60% – 80% decline in the economy, owing to lockdown, in a very short period of a month or six weeks.

So far, no matter what the national strategy (or lack of one, as in the US) — herd immunity (Sweden), local lockdown (Italy), school-opening and back-to-normal prematurely (US) — economies are plateau-ing, at 60% to 80% of their previous pre-pandemic level. And in most of the 10, COVID-19 is making a comeback, in a second or third wave — with the age of those infected declining sharply, as young people emerge, head to bars, and parties, and colleges – and become ill.

And, if that isn’t bad enough, a new forecast from the leading pandemic prediction institution, at Univ. of Washington, reports this: A new long-term forecast predicts a significant acceleration in Covid-19 deaths in the U.S. as colder weather takes hold. Under the latest projections from the Institute for Health Metrics and Evaluation at the University of Washington’s School of Medicine, deaths could rise to 410,000 by the end of 2020. In a worst-case scenario, there could be 620,000 fatalities, more than three times the number of Americans who have died over the past eight months. The difference between the projected and worst-case scenarios comes down to how diligent authorities are in mandating masks and social distancing, according to the report.

Readers, fasten your seat belts. Many of us yearn for the good old days, like, those we have 6 months ago. It does not seem likely any time soon. Prepare yourself and your family for a rocky road to recovery. It will be a marathon, not a sprint. Even optimistists believe an effective vaccine won’t be available for many months – and then, how many vaccine-deniers will turn it down, lacking trust in leaders who follow politics rather than science?

Managing COVID-19 Tradeoffs: An Economic Lesson by a Pediatrician

By Shlomo Maital

Well, it took a pediatrician to teach everyone a simple, powerful lesson in Economics. The pediatrician is Aaron E. Carroll, and he is Professor of Pediatrics at the Indiana University School of Medicine. His Op-Ed in today’s global New York Times * makes an important point.

“…as we loosen restrictions in some areas, we should be increasing restrictions in others.”

Simple? Obvious? As kids go back to school today, and joyously huddle with their friends, whom they haven’t seen for ages, the assumption is, if we’re clustering together in school, it’s OK to cluster together everywhere.

It’s a free lunch. The logic is “both-and”. Both at school, and at home, and at parties, and …everywhere. Both-and is today’s social norm. We want it all.

But there is a tradeoff at play here. If you take more risk in school, then you have to take less risk elsewhere, because – we cannot let risk rise infinitely, it is a kind of resource that is fixed in amount, and if we use too much of it, it will for sure come back and bite us hard…

This is a very hard lesson for everyone to swallow, especially when the feeling is: We’ve quarantined, social-distanced for so long – now it’s over, time to huddle and cluster and gather.

Not so. The second wave of COVID-19 has occurred mainly because of this false assumption.

So let us each of us take responsibility and manage our risk tradeoffs. The question should be: what am I doing, that increases the risk of infecting myself and others? What can I do to reduce that, so that when I do join 10 others for prayer or socializing, my risk allocation is not excessive.

Long ago, I taught managers a useful tool for managing business tradeoffs, known as “Even Swaps”, co-invented by Harvard Professor Howard Raiffa, a game-theory expert.** The idea here is simple. List all your options. Discard those that are ‘dominated’, that is – all other options are better in every way. This is easy.

Next part is hard. For the remaining options, list the six common things for each that bring you joy. Score each 1 to 5, with 5 being “most joy”. Now — a short cut (Raiffa’s approach is more complex): Imagine yourself choosing each option: A, B, C…. and ask which– brings more joy? (Note: joy is not happiness…it is less ephemeral, less transient, deeper, with more meaning).

And a supplemental tool. Of all the things I am now doing – ask yourself, which can I stop doing, totally, and as a result, find greater joy? In new product development, ‘addition’ (what feature can we add?) creates cluttered, costly, complicated, unfriendly devices. Best to start with subtraction: What can I REMOVE from this device, to make it better, friendlier, simpler, cheaper? The same works in life. What can I stop doing? Specifically, what can I stop doing, that reduces risk of becoming infected and infecting others?

The notion of giving up things we like is a tough one for modern society. Climate change policy, and its failures, are proof. But in a pandemic, as Dr. Carroll points out, recognizing trade-offs and managing them are vital. Thanks, Doc! It took an MD to explain some basic Economics.

* “Most of us have the risk of COVID-19 exactly backwards”. Sept. 1, P. 11

** J S Hammond, R I Keeney, Howard Raiffa. “Even swaps: A rational method for making trade-offs”. Harvard Business Review, March-April 1998.